Defense is moving back to the center of the market conversation, but the important shift is not simply geopolitical fear. It is the realization that allied rearmament is becoming an industrial cycle with visible order books, factory constraints, and supplier bottlenecks. Reuters reported on June 25 that NATO Secretary General Mark Rutte said billions of dollars in new defense contracts would be announced around the summit. That matters because once defense demand is framed as signed business instead of vague strategic urgency, traders start valuing backlog quality, production speed, and supplier positioning rather than just headline risk.

The policy signal is getting harder to ignore. NATO’s June 2026 defense-investment messaging centered on a much bigger burden-sharing target and on faster production across the alliance. In practical terms, that means the market now has to think about whether the West can physically manufacture enough interceptors, radars, launch systems, armored vehicles, and electronics to support a multi-year replenishment cycle. This is why the trade feels broader than a single prime contractor story.

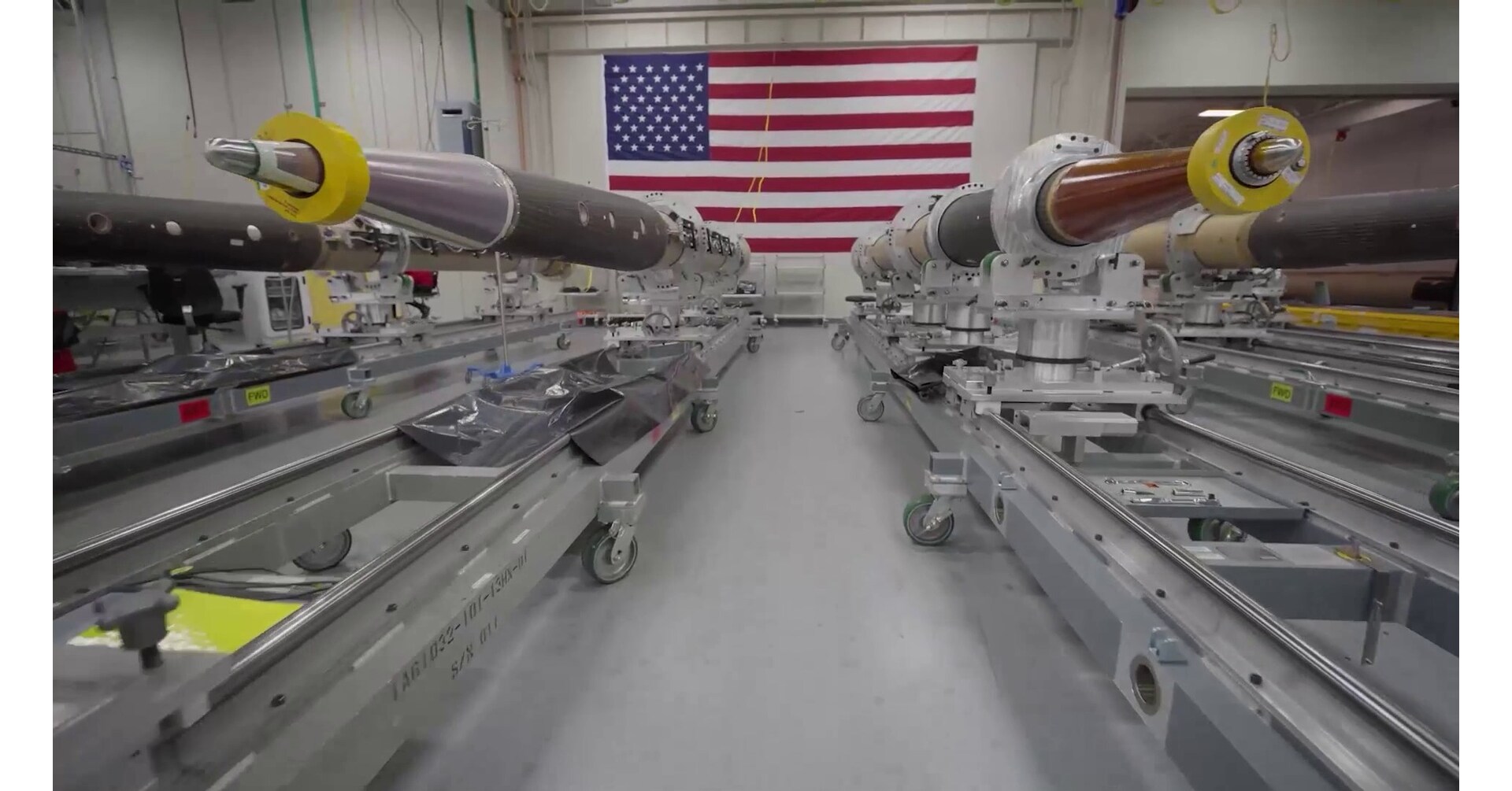

The United States offered the cleanest proof point this week. Lockheed Martin said on June 24 that it had received a $35 billion, seven-year procurement award tied to THAAD interceptor production. Europe is giving the same message from another angle: Rheinmetall said on June 2 that it had secured a 5.7 billion euro historic contract in Romania. South Korea is trying to turn that demand wave into market share. Hanwha used BSDA 2026 to emphasize deeper European partnerships and to showcase the kind of systems that sit directly inside the rearmament queue. Japan is not standing aside either. Mitsubishi Electric said on April 28 that it would participate in Japan-U.S. co-production related to the AMRAAM missile framework, a reminder that Japanese listed defense suppliers can benefit even when the immediate contract headlines are centered elsewhere.

That combination creates a credible cross-market signal across the United States, Europe, Japan, and Korea. Traders are discussing defense again because this is no longer only a macro-security theme. It is also a manufacturing theme. The winners may be the companies that can localize output, secure components, and shorten delivery schedules, not just the names with the most recognizable weapons brands. In that sense, defense is beginning to trade more like power equipment, semiconductors, or aerospace engines: capacity matters, certification matters, and timeline credibility matters.

My cautious view is that the market is right to take this backlog cycle seriously, but it should not assume a straight-line rally. Defense names can look irresistible when governments talk bigger, yet margins, delivery timing, export approvals, and coalition politics still matter. A long order book is supportive, but it can also hide execution risk if factories, labor, or subcomponent supply fail to scale as quickly as investors expect.

The cleaner interpretation is that allied rearmament has moved from a headline trade toward a production trade. If that continues, U.S. missile-defense exposure, European armored-vehicle and ammunition capacity, Japanese electronics and missile-component suppliers, and Korean artillery-and-systems exporters can all stay in focus together. But this remains a policy-driven sector. When valuations move faster than production, pullbacks can arrive just as quickly as the contracts.

Risk notice: This article is for market commentary and information only. It is not investment advice, not a recommendation to buy or sell any asset, and not a guarantee of future results. Stocks, futures, commodities, currencies, and crypto-linked assets can react sharply to defense-policy changes, procurement delays, export restrictions, and geopolitical events.

Sources:

Reuters syndication: Rutte says billions in new defense contracts will be announced at summit

NATO: press conference on defense investment and summit priorities

Lockheed Martin: $35 billion THAAD seven-year procurement award

Rheinmetall: Romania contract worth 5.7 billion euros

Hanwha: BSDA 2026 European partnership push

Mitsubishi Electric: participation in Japan-U.S. AMRAAM co-production framework

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/451