The handset market has turned into one of the more interesting second-order AI trades. On June 1, 2026, Reuters reported that Counterpoint now expects global smartphone shipments to fall 13.9% this year, the steepest annual contraction on record, as memory shortages worsen and low-end devices become harder to build profitably. That is not just a consumer-demand story. It is a capital-allocation story: memory supply is being pulled toward AI infrastructure, and the cheap end of the smartphone market is paying the bill.

For U.S. traders, the obvious read-through is that Apple looks more like a relative winner than a cyclical victim. Counterpoint’s view is that Apple can keep 2026 shipments roughly flat and even return to growth next year because it still has pricing power, loyal upgrade demand, and better supply security than weaker Android peers. That does not make the stock cheap or risk-free, but it does mean the market may continue rewarding ecosystem strength over unit volume.

South Korea is where the split gets more dramatic. Reuters reported on April 30 that Samsung’s chip profit exploded on AI-driven memory demand even as its mobile division prepared for weaker profitability because component costs are rising too fast. In other words, Samsung can make more money from the shortage that is simultaneously making phones harder to sell. That tension matters for traders watching both Samsung Electronics and the wider Korea tech complex: the memory winners and the handset assemblers are no longer moving in lockstep.

Japan adds a different signal. Reuters reported on May 8 that Sony and TSMC plan a new Japan joint venture for next-generation image sensors, with spending phased by demand and backed by the logic that premium hardware still deserves investment. I read that as a bet that even in a shrinking handset market, the winners will still pay for better cameras, sensors, and differentiated components. Japan’s trade is less about unit growth now and more about owning the profitable layers that survive the volume washout.

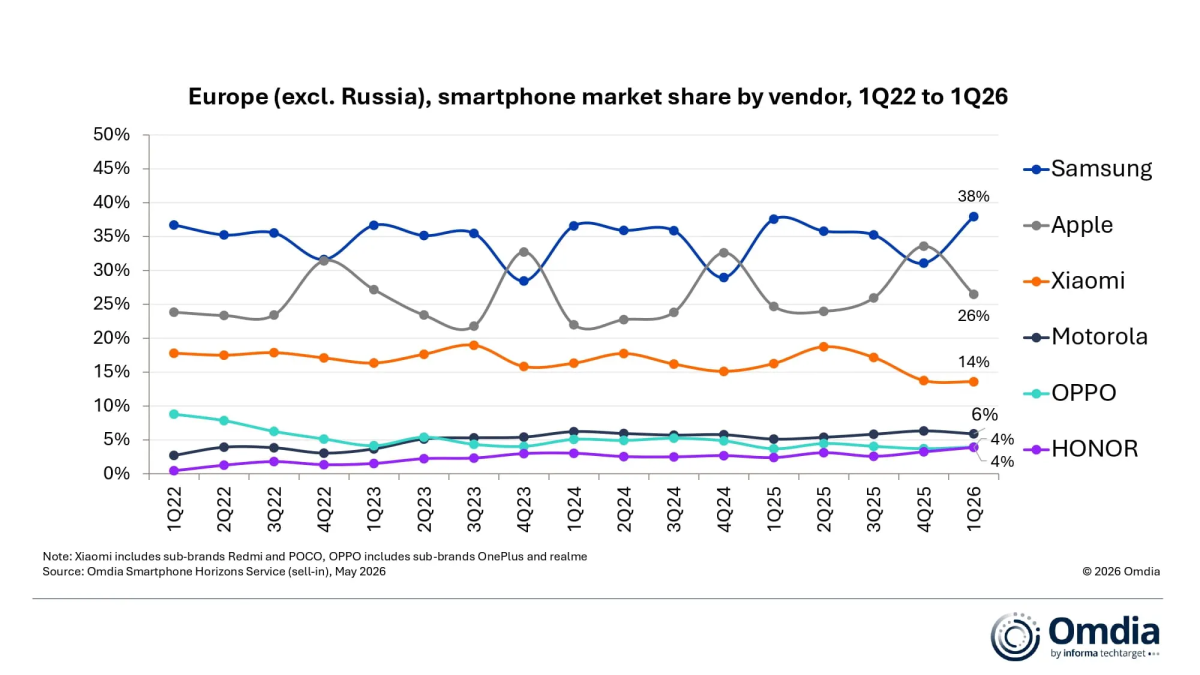

Europe is the market where that premium-versus-volume split is becoming visible in the channel. SamMobile, citing Omdia data published in late May, said Samsung held the top spot in Europe in Q1 2026 while Apple stayed strong and Xiaomi weakened. That does not prove Europe is healthy. It suggests Europe is rewarding scale, financing power, and recognizable premium brands while squeezing mid-tier challengers. For traders, that is a tougher and more selective backdrop than the old broad handset recovery thesis.

The bearish part of this setup is straightforward: Reuters reported in February that Qualcomm and Arm were already feeling weaker smartphone-chip demand because customers could not secure enough memory to ship finished devices. If the memory shortage stays tight into 2027, the pain spreads from handset brands into the broader mobile silicon stack. My cautious view is that this remains a barbell market. Premium ecosystems, memory pricing power, and differentiated components can keep working, but the old assumption that all smartphone names rally together looks broken.

Risk notice: This article is for market commentary only, not personalized investment advice. Technology supply chains, pricing, geopolitics, and consumer demand can change quickly, and volatile stocks can move sharply in either direction.

Sources: Reuters on Counterpoint’s June 1 smartphone forecast; Reuters on Samsung’s April 30 chip profit and mobile-margin squeeze; Reuters on Sony and TSMC’s Japan image-sensor venture; SamMobile citing Omdia on Europe Q1 smartphone share; Reuters on Qualcomm and Arm exposure to the handset slowdown; Reddit trader and consumer discussion on the handset squeeze.

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/174