The aviation trade is quietly changing shape. The obvious headline is still aircraft demand, but the more interesting market signal is that repair capacity, engine turnaround time, and shop throughput are starting to matter as much as fresh order books. When the constraint moves from selling planes to keeping engines moving, the winners and losers can shift fast.

The freshest proof came on July 2, 2026. Reuters reported via TradingView that Airbus delivered 350 aircraft in the first half of the year even as supply-chain problems remained a drag. Airbus had already said in its first-quarter results that it would keep ramping production while navigating shortages of Pratt & Whitney engines. That is an important distinction for traders. Demand is not the main question. The system is trying to work through a maintenance-and-components choke point.

In the United States, Pratt & Whitney is reacting with capacity, not slogans. RTX said on April 21 that Pratt & Whitney would invest more than $100 million across MRO sites in Texas, Florida, and Arkansas to expand GTF engine maintenance capacity and improve turnaround efficiency. If a company is putting nine figures into repair infrastructure, that tells you the bottleneck is not theoretical anymore.

Europe is seeing the same pressure from a different angle. MTU said on April 22 that its Hannover operation was marking 10 years of Pratt & Whitney GTF engine MRO, a reminder that the installed base is now large enough for maintenance capacity itself to become a tradable theme. This is why aerospace investors have to separate demand from conversion. Air travel can stay solid while airline and supplier economics still get squeezed by grounded aircraft, engine removals, and long shop queues.

Japan’s read-through is not just airline traffic but industrial capacity. IHI’s May 8 management material said it wants to capture immediate demand through steady expansion in the civil aero-engine business and to expand supply capacity to meet that demand. That sounds dry, but the implication is clear: Japanese industrial groups also see civil aero engines as a real capacity opportunity, not a side story.

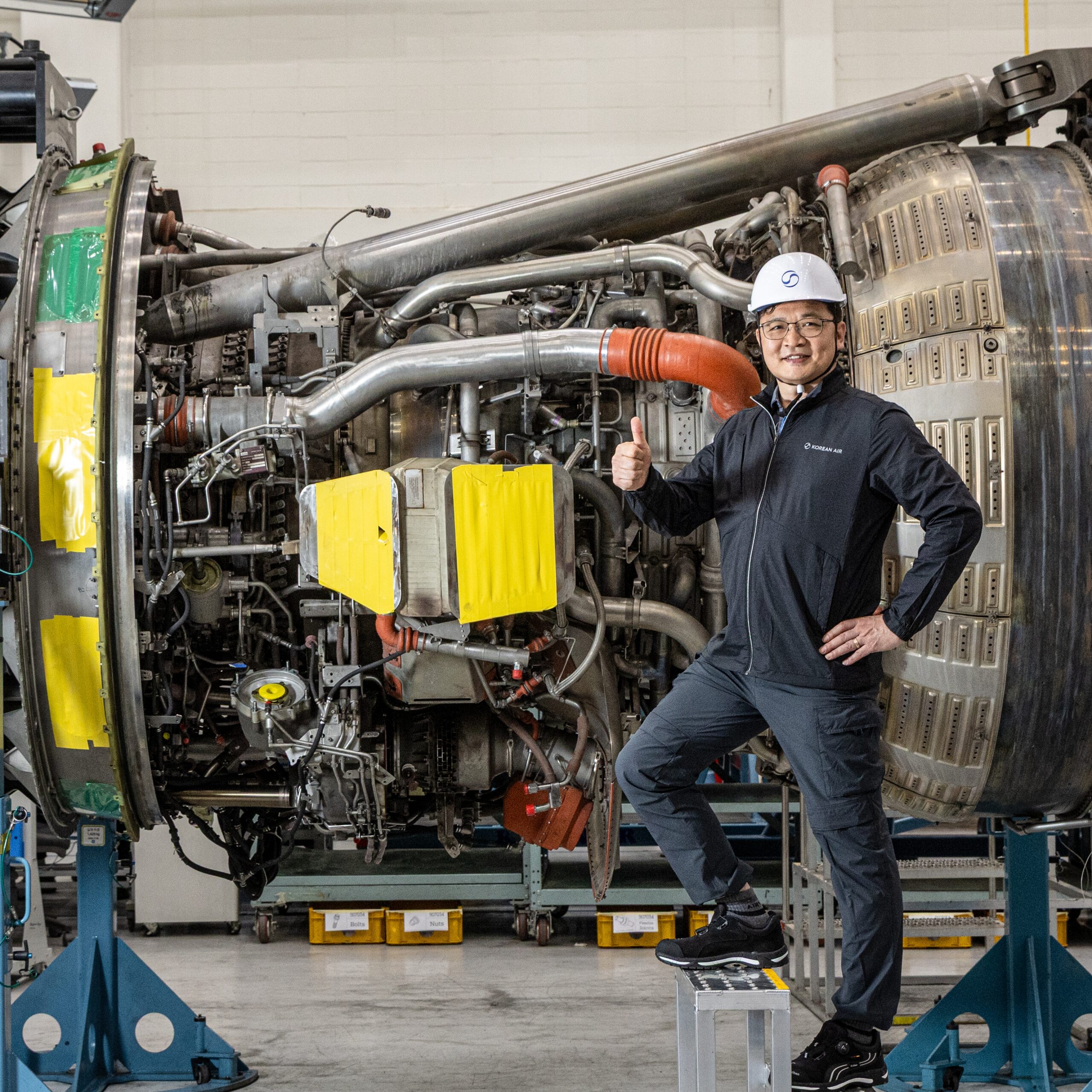

South Korea offers the maintenance-floor version of the same thesis. Korean Air’s April 30 newsroom feature on its engine test cell walked through the final validation process before an overhauled engine goes back into service, underscoring how critical scheduling, parts supply, and final performance checks have become. In other words, this is not just about glamorous OEM headlines. It is about who can actually return engines to the wing without losing months.

My cautious market view is that this is a better execution trade than a pure demand trade. The bullish case is easy to understand: healthy aircraft demand, rising installed engine fleets, and long-duration aftermarket revenue. The harder question is whether suppliers and MRO networks can turn that backdrop into cleaner delivery cadence and shorter repair cycles. If not, the theme stays attractive but messy, and aerospace names can still disappoint even when the top-line demand story looks fine.

The cross-market signal is unusually consistent. Airbus is still working through supply strain, U.S. engine makers are spending to widen shop capacity, European MRO players are celebrating scale because the queue is real, Japan wants more civil aero-engine throughput, and Korea is emphasizing maintenance execution. That is why aviation is starting to trade less like a simple plane-order story and more like an engine-shop bottleneck story.

Sources

Reuters via TradingView: Airbus delivered 350 planes in the first half amid supply-chain strain

Airbus Q1 2026 results

RTX / Pratt & Whitney: more than $100 million to expand U.S. MRO footprint

MTU: 10 years of Pratt & Whitney GTF engine MRO

IHI: management overview on civil aero-engine capacity expansion

Korean Air Newsroom: engine test cell feature

Risk notice: This article is for market commentary only, not personal investment advice. Aerospace, airline, engine, and industrial stocks can be volatile, and repair delays, parts shortages, tariff changes, certification issues, and macro demand slowdowns can reverse sentiment quickly.

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/511