The semiconductor trade is starting to move one layer upstream. For most of the last year, investors chased the obvious winners: GPUs, HBM memory and anything attached to AI server demand. Now the market is paying more attention to the tools, process steps and packaging constraints that decide who can actually turn that demand into shipped silicon. That is a different trade. It is less about pure narrative beta and more about who controls the narrowest parts of the manufacturing funnel.

Europe is setting the tone through ASML. Reuters reported on May 19 that ASML expects the first chips made with its next-generation High-NA EUV systems to arrive within months. That matters because the market has been debating whether High-NA was still mostly a science-project expense. ASML’s message was more practical: the equipment is expensive, qualification is hard, but the point is to lower patterning costs over time. Once investors believe the next lithography step is moving from promise to product, the discussion shifts from abstract AI enthusiasm to hard capex, yields and adoption timing.

The U.S. angle is equally important. Reuters reported on May 22 that U.S. Trade Representative Jamieson Greer saw no immediate semiconductor tariff coming, but stressed that protection for domestic production remains important while the reshoring phase plays out. In the same report, Micron said it had begun 1-alpha DRAM wafer manufacturing in Virginia and was expanding total planned U.S. investment to $200 billion. That combination tells traders something useful: Washington still wants local chip capacity, but it also knows this supply chain cannot be rebuilt instantly. The factory race is real, but it still needs time, imported equipment and a lot of execution.

Korea is giving the cleanest proof that the cycle is already flowing through real trade numbers. Reuters reported on June 1 that South Korean semiconductor exports jumped 169.4% year over year in May to a record monthly high, with overall exports rising at the fastest pace in more than four decades. That is not just a good headline for chip bulls. It is evidence that the manufacturing bottleneck is being monetized now, especially for memory and AI-server-linked suppliers. When export data accelerates that sharply, traders stop treating semiconductor infrastructure as a distant theme and start treating it as current earnings power.

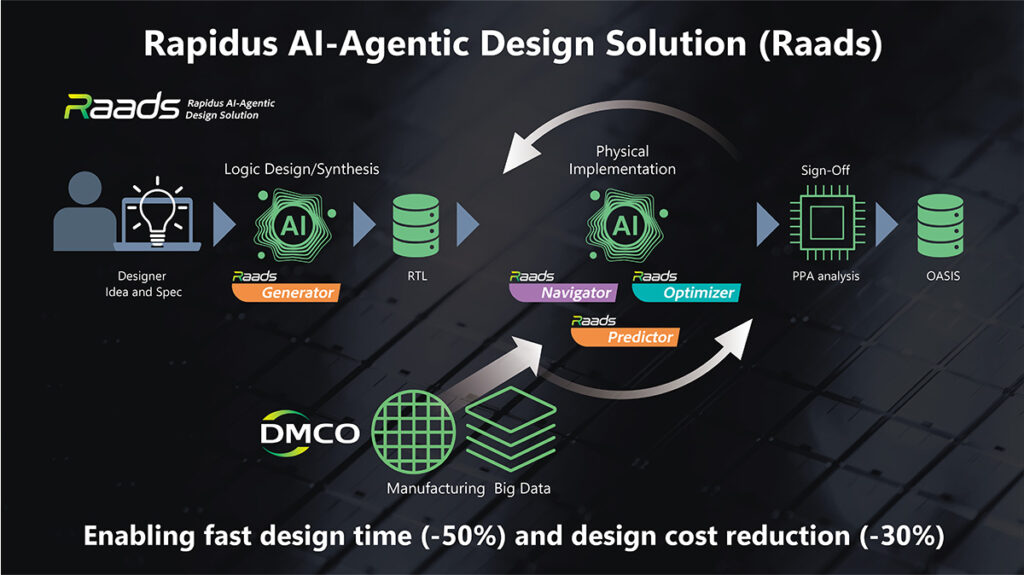

Japan’s contribution is more strategic but no less important. Fujifilm said on February 27 that it completed a 5 billion yen investment in Rapidus and is expanding materials capacity in Japan to support leading-edge domestic semiconductor production. Rapidus itself has been framing the race around shortening cycle times across design, wafer processing and 3D packaging, not just around owning a headline node. Even retail discussion is picking up the same point. In a recent Reddit hardware thread reacting to the ASML news, commenters quickly shifted from the machine itself to package size limits, EMIB, and how future AI parts may need packaging changes as much as lithography improvements. That is exactly the market signal I care about: the conversation is migrating from chips as products to semiconductors as a constrained industrial system.

My view is that this is a healthier semiconductor trade than the pure momentum versions we saw earlier. When the market starts rewarding lithography, packaging, materials and process control, it usually means investors are thinking more seriously about the physical limits of scaling. The risk is obvious: these names can get over-owned fast, and technical milestones do not always become clean earnings stories on schedule. High-NA adoption could slip, subsidies can turn political, and packaging ambitions can outrun commercial demand. Still, the cross-market read is clear. The bottleneck has moved upstream, and that is where a meaningful part of the next semiconductor rerating may come from.

Risk notice: This article is for market commentary only, not personalized investment advice. Semiconductor, equipment, materials and advanced-packaging names can be volatile and may react sharply to capex cycles, export controls, subsidy changes, execution delays, customer concentration and valuation compression. Traders can lose money quickly.

Sources:

1. Reuters via Investing.com on ASML expecting first High-NA products within months (May 19, 2026): https://www.investing.com/news/stock-market-news/asml-says-first-chips-from-new-highna-machines-to-arrive-in-months-4698075

2. Reuters via Investing.com on USTR Greer, Micron and the timing of semiconductor protection (May 22, 2026): https://m.investing.com/news/economy-news/ustr-greer-sees-no-immediate-chip-tariffs-but-says-protection-important-for-sector-4707278?ampMode=1

3. Reuters via Investing.com on South Korea’s record chip-led export growth (June 1, 2026): https://www.investing.com/news/economic-indicators/south-korea-export-growth-hits-fourdecade-high-as-chip-sales-hit-record-on-ai-boom-4717976

4. Fujifilm on its investment in Rapidus and expanded semiconductor-material support in Japan (February 27, 2026): https://www.fujifilm.com/us/en/news/fujifilm-completes-investment-in-rapidus

5. Rapidus on design-cycle reduction across 2nm manufacturing and 3D packaging tools (December 17, 2025): https://www.rapidus.inc/news_topics/news-info/rapidus-unveils-new-ai-design-tools-for-advanced-semiconductor-manufacturing-2/

6. Reddit hardware discussion reacting to the ASML High-NA report and package-size constraints (May 20, 2026): https://www.reddit.com/r/hardware/comments/1tic9pu/asml_says_first_chips_made_with_highna_euv/

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/297