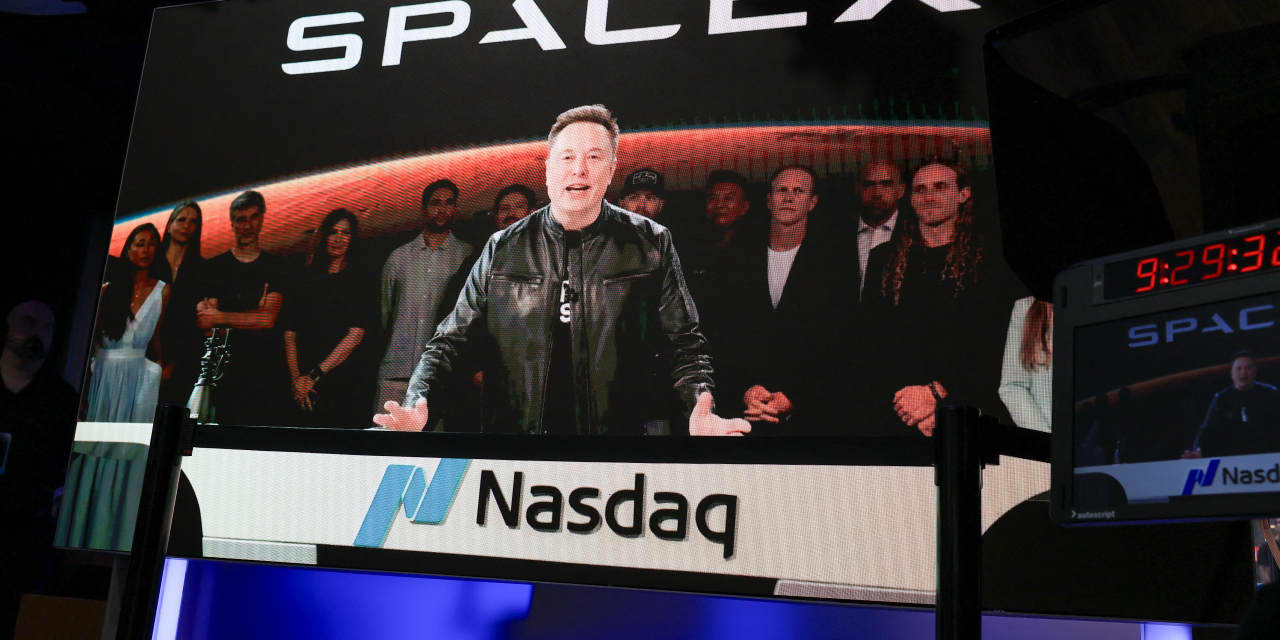

Traders are no longer treating space as a distant concept stock story. After SpaceX’s June 12 Nasdaq debut closed about 19% above its IPO price and pushed its market value above $2 trillion, the market suddenly had a fresh price anchor for launch, satellite connectivity and orbital infrastructure. That matters well beyond one U.S. ticker, because it forces every listed space-adjacent name in developed markets to answer the same question: do you have real launch cadence, real industrial capacity, or just a narrative?

Japan added the most important non-U.S. proof point on the same day. JAXA said the H3 flight No.6 test vehicle launched successfully on June 12, while the agency’s H3 program page stresses flexibility, reliability and lower cost as the commercial target. AP’s June 12 report also highlighted that this mission introduced a lower-cost configuration and helped restore momentum after earlier failures. For Japanese industrials, that is the difference between having a national prestige project and having something the market can begin to handicap as a usable launch platform.

Europe’s angle is less about headline frenzy and more about supply discipline. ESA said on June 9 that Luca Parmitano will pilot Artemis III and that Europe is supplying the third European Service Module for Orion. That confirms Europe is still deeply wired into the highest-visibility human-spaceflight program. More importantly for traders, Mitsubishi Electric said on March 4 that it invested 50 million euros in Spain’s PLD Space to secure small-satellite launch resources and priority access to MIURA 5. When industrial groups start paying up for launch slots before revenue fully lands, the market signal is obvious: scarce access to orbit is becoming a bottleneck, not a side detail.

Korea fits the same theme even if its listed route is less direct. Yonhap reported on June 12 that Hanmi Semiconductor plans to buy 50 billion won of SpaceX shares ahead of the debut, a sign that Korean capital is trying to get exposure to the orbit stack rather than ignoring it. At the state level, KASA also said this month that Korea’s first mass-produced low Earth orbit satellite made initial contact and is moving toward a full observation mission in July. Put together, the Korean angle says the country is not just watching U.S. space valuations from the sidelines; it is trying to plug into the ecosystem through both capital and hardware.

My view is that this is a real theme, but it is not a blank check for every ‘space’ label. SpaceX’s IPO may lift sentiment, yet it also raises the bar. The likely winners are companies tied to launch capacity, satellite manufacturing, propulsion, mission hardware and sovereign communications programs. The likely losers are names that only trade on association and cannot show contracts, launch windows or industrial execution. Cross-market, this looks more like an infrastructure scarcity trade than a meme bubble, but scarcity trades become dangerous when investors stop distinguishing between platforms and passengers.

Risk notice: This article is market commentary for information only, not personalized investment advice. Space, defense and high-growth technology names can be extremely volatile, and policy, launch, regulatory and execution setbacks can change sentiment quickly.

Sources:

MarketWatch: SpaceX IPO live coverage

JAXA: H3 Launch Vehicle

AP: H3 rocket returns to flight

ESA: Luca Parmitano joins Artemis III as pilot

Mitsubishi Electric: Invests in PLD Space

Yonhap: Hanmi Semiconductor to acquire SpaceX shares

KASA: Initial contact successful for Korea’s first mass-produced LEO satellite

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/393