One of the cleaner market-structure trades right now is not a sector, a commodity or a single macro view. It is the idea that exchanges and listed-derivatives venues are steadily taking ownership of more hours in the day. That matters because when volatility refuses to stay inside old cash-market sessions, the venues that capture overnight hedging flow, weekend price discovery and extended-hours options activity become more strategically valuable.

The U.S. side is the easiest place to see the shift. CME Group said on June 1 that it launched 24/7 trading for cryptocurrency futures and options, with the new schedule already producing more than 7,200 contracts in its inaugural weekend. That is a small number relative to flagship rates or equity-index franchises, but the direction matters more than the first print. It is regulated derivatives infrastructure moving closer to crypto’s natural clock rather than forcing crypto risk back into a legacy schedule. Cboe then added another sign on May 28, saying the SEC approved its plan to offer extended trading hours for select multi-listed single-stock options, including a pre-market session from 7:30 a.m. ET to 9:25 a.m. ET and a short post-market session after the close.

Europe’s angle is not just about staying competitive with U.S. exchanges. Eurex said it obtained permission to offer MSCI Korea Index futures during Asian trading hours, aligning the product with other MSCI index futures from March 30, 2026. That is a useful signal because it shows a European venue trying to monetize Asian risk when Asian investors are actually awake, instead of pretending regional exposure should wait for Europe to open. Cross-time-zone derivatives liquidity is increasingly becoming a product-design issue, not just a technology issue.

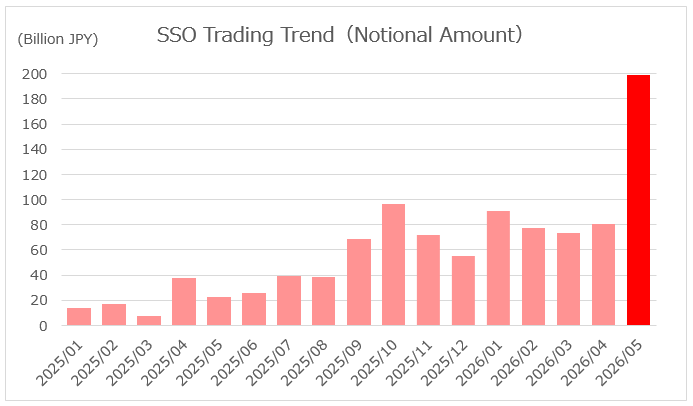

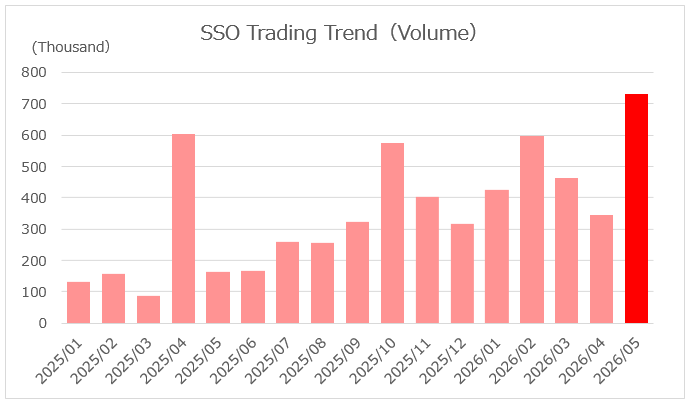

Japan already has the proof that longer trading windows can turn into real activity rather than just a marketing slogan. JPX said FY2025 night-session volume reached 182.8 million contracts, or 41.5% of total derivatives volume, and the ratio rose to 48.7% in March 2026. JPX also reported record monthly notional amount and volume for Osaka Exchange single-stock options in May 2026. That combination is important. It suggests the exchange story is no longer limited to benchmark index futures. Activity is broadening into more granular listed hedges, which usually means users are becoming more comfortable managing risk outside the old daytime-only routine.

Korea is moving in the same direction with more explicit infrastructure language. KRX’s April 2025 guide to its derivatives night session says the exchange completed preparations for the first night session in the history of the Korean capital market, while also noting Korea had built experience through cooperation with CME and Eurex since 2009. The product menu spans stock-index, rates, currency and commodity derivatives. My read is that Korea is not just following a global fashion. It is trying to reduce the gap between when Korea-related risk happens and when Korea-based investors are allowed to hedge it.

My cautious view is that this is a better exchange-equity and market-plumbing story than a simple directional call on the underlying assets. The bullish case is obvious: more hours, more event coverage, more hedging demand and potentially stickier data and clearing economics. The risk is that longer sessions fragment liquidity, raise operating costs and create the appearance of access without enough depth in the most important names. Even so, traders are right to keep watching this. The next leg of the derivatives business may come less from inventing exotic products and more from refusing to let the tape sleep.

Risk notice: This article is market commentary for information only, not personalized investment advice. Exchange operators, brokers and derivatives-linked names can react sharply to regulation, trading-volume swings, product-adoption disappointments, cybersecurity incidents and volatility shocks.

Sources:

CME Group: Launch of 24/7 cryptocurrency futures and options trading

Cboe: SEC approval for extended trading hours in select single-stock options

Eurex circular: Extension of trading hours for MSCI Korea futures

JPX: Trading overview in FY2025 and March 2026

Osaka Exchange: Single-stock options recorded all-time highs in May 2026

KRX: Guide to Night Session in KRX Derivatives Market

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/402