The market keeps talking about oil as a macro input, but for airlines the sharper signal is now jet fuel and what it does to route economics. Europe offered the clearest update on June 5: the European Union said it does not see an immediate jet-fuel shortage, yet airlines are already cutting routes that no longer make economic sense. That matters because it shifts the story from panic about empty tanks to a more tradable question about who has pricing power, hedges and network discipline.

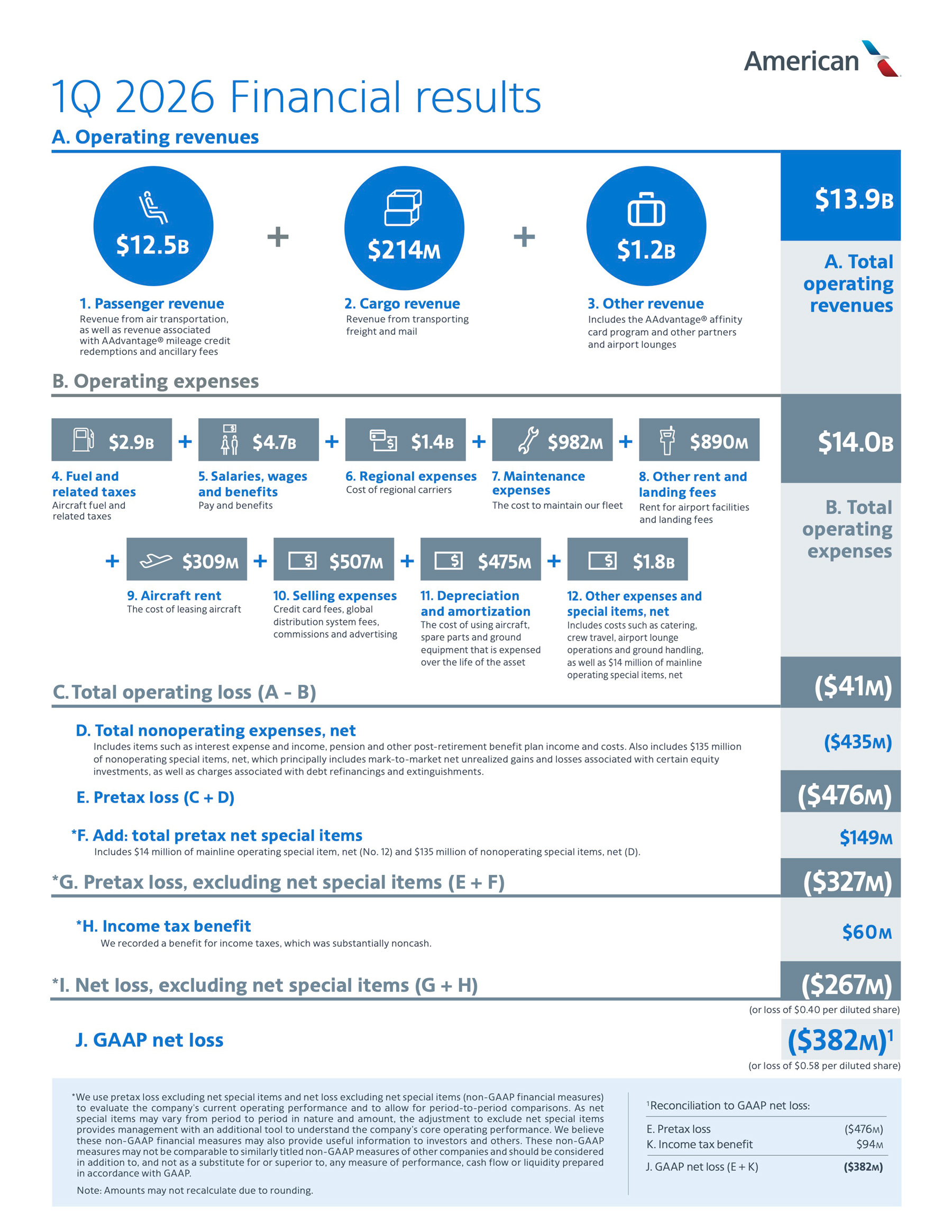

My read is that this is not a broad airline short by default. It is a separation trade. Reuters’ airline factbox shows exactly how uneven the pressure is: Delta and United are cutting capacity and raising fees, American says its 2026 jet-fuel bill could rise by more than $4 billion, while weaker leisure and low-cost operators are trimming flights more aggressively or warning that margins are getting crushed. When fuel stays expensive, the winners are usually the carriers that can remove marginal capacity without damaging their franchise.

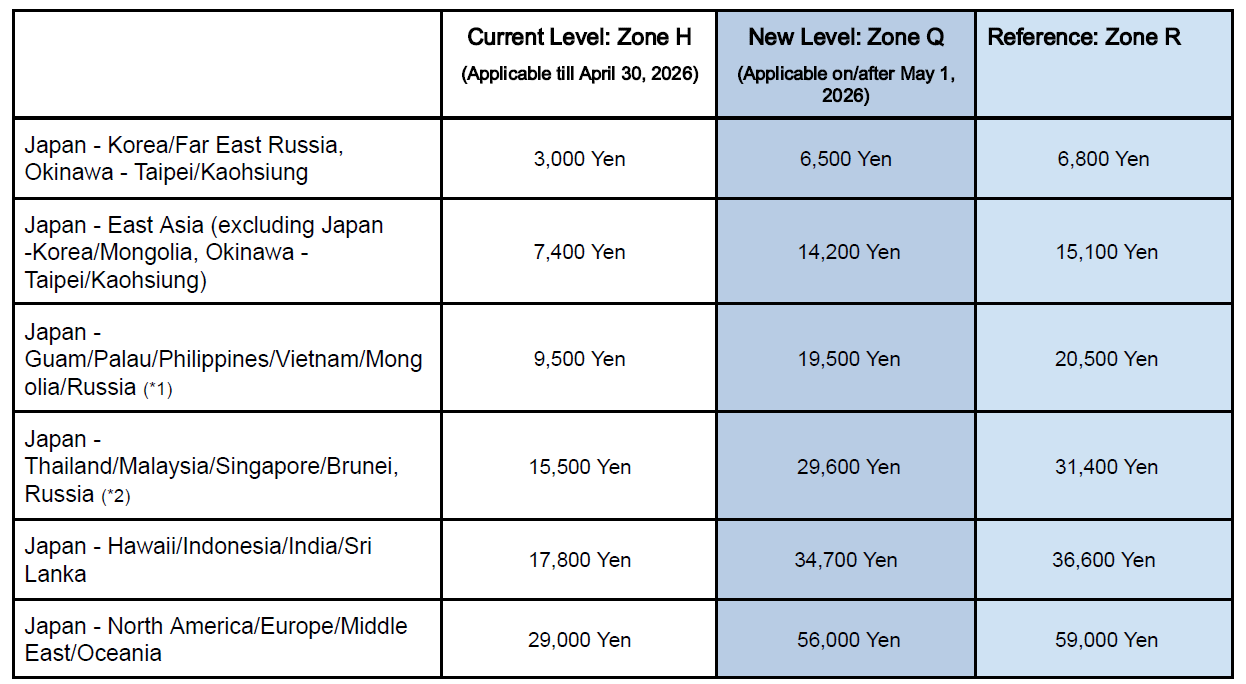

Japan fits that logic well. Japan Airlines said the average Singapore kerosene price in February and March was about $146.99 per barrel, high enough to justify an elevated fuel-surcharge zone for May and June ticket issuance even after government mitigation measures softened the hit slightly. In other words, Japan is not trading on a collapse scenario. It is trading on normalized expensive fuel, which is arguably more durable and more important for earnings models.

South Korea is slightly different, but not bullish in a carefree way. Reuters reported Korean Air entered emergency management mode earlier in the spring, and Korean Air’s June cargo notice still shows fuel well above normal even after retreating from the March-April spike. The newest cargo surcharge schedule falls versus the previous period, but it remains high enough to tell you that Korean aviation and export logistics are still operating in a fuel-stressed regime, not a clean recovery regime.

The cross-market signal is straightforward: this is becoming a balance-sheet and yield-management trade, not a pure passenger-volume trade. Europe may avoid a physical shortage, the U.S. majors may claw back part of the pain, Japan may manage with surcharges, and Korea may keep squeezing efficiency, but none of that means the pressure has disappeared. My cautious view is that investors should treat airline strength selectively and keep watching whether high fuel turns into durable fare power for network carriers or simply destroys demand on the margin.

Risk notice: This article is for market commentary only, not investment advice. Fuel prices, hedging outcomes, route decisions, geopolitical risks and travel demand can change quickly, and airline, refinery and transport stocks can be highly volatile.

Sources:

Reuters via MarketScreener – EU sees no jet fuel shortage amid price surge, transport chief says (June 5, 2026)

Reuters via Investing.com – Airlines tackle fuel cost surge with price hikes and outlook cuts (May 15, 2026)

American Airlines – First-quarter 2026 financial results (April 23, 2026)

JAL – International fare fuel surcharge for tickets issued between May and June 2026 (April 20, 2026)

Korean Air – June 2026 cargo fuel surcharge notice (June 1, 2026)

原创文章,作者:financial transaction,如若转载,请注明出处:https://www.fanbi.net/archives/258